ESG at portfolio level

We are aware of the environmental impact of our business activities and are committed to contributing to a green economy through our lending and investing in sustainable development. In addition to reducing our own carbon footprint, we also want to help our customers minimising their climate impact.

The financial sector plays a crucial role in the sustainability transformation and in combating climate change. The following section summarizes HCOB’s activities to reduce financed emissions and to decarbonize its portfolio. We are working to transparently disclose climate impacts and to gradually align our lending and investment portfolio with the defined decarbonization targets.

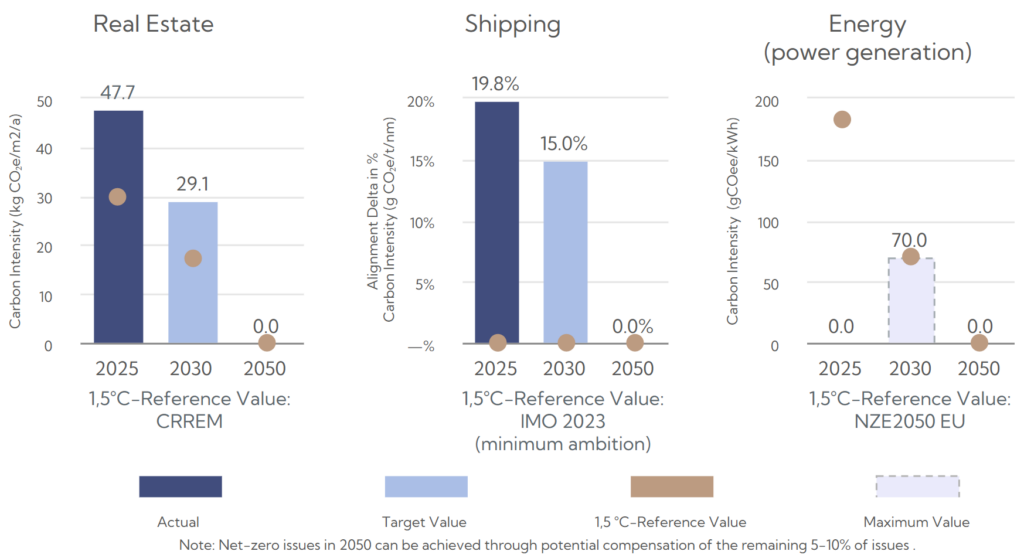

Decarbonization targets for the portfolio

By signing the UN Principles for Responsible Banking (PRB), HCOB has committed itself to the goals of the Paris Climate Agreement and aims to achieve net zero emissions across its entire lending and investment portfolio by 2050. In addition, decarbonization targets for 2030 and 2050 apply to the sub portfolios Real Estate, Shipping, and Energy (power generation).

Our financed emissions

HCOB is committed to measuring and disclosing its greenhouse gas emissions by signing the commitment to the industry wide standards of the Partnership for Carbon Accounting Financials (PCAF). In doing so, the Bank aims to enhance transparency regarding its climate impacts. Below you will find an overview of the Bank’s financed emissions as of 31 December 2023.

Financed Emissions, Sector View (31.12.2025)

| Business segment | Covered loan amount total € million | Financed emissions t CO2e Scope 1 & Scope 2 |

| Real Estate | 5,875 | 126,042 |

| Global Transportation | 2,457 | 1,569,352 |

| Project Finance | 3,769 | 189,477 |

| Corporates | 3,793 | 302,560 |

| Treasury | 111 | 405 |

| Total | 16,005 | 2,187,835 |

HCOB´S ESG linked Screening & Classification Process

As a bank, we are aware of our environmental impact and are committed to sustainable lending and investments. To this end, we follow the following approach in all lending processes in accordance with the Paris Climate Agreement, the Sustainable Development Goals (SDGs), the PRB, the EU Taxonomy and the Task Force on Climate-related Financial Disclosures (TCFD) recommendations:

Compliance Assessment & Sector Restrictions Check

As a part of HCOB’s decision process for conducting new business relationships, the Compliance Assessment & Sector Restrictions Check must be performed. It consists of two levels and defines the overall legal, regulatory and ethical framework as well as the strategic limitations for HCOB‘s business activities.

In this way, we ensure a thorough examination of new business. We take various factors into account, such as the location of a project, the borrowers or companies and donors, as well as their fundamental ethical principles and respect for human rights.

The ESG Scoring

Our ESG scoring includes a thorough analysis of the climate, environmental, social and governance risk factors for each financing. For credit decisions, there are ESG scoring grades from one to six, with one being very good and anything after four leading to regular exclusion from the commitment.

Sustainable & Transformational Finance Framework

STFF is a classification system for categorising our lending business as “sustainable” or “transformational”. The assessment is carried out against the background of the requirements of the EU taxonomy, among other things, and creates transparency with its comprehensive and consistent approach.

Decision of the Credit Committee

Every credit decision goes through the Credit Committee at the end of the decision-making process. Every new business is presented to the committee and then either approved or rejected. In principle, an ESG scoring of 5 or 6 leads to exclusion from lending, unless risk-minimising factors are presented and the transaction is expressly accepted by members of the Credit Committee with voting rights.

For detailed information on ESG in the credit & investment process click here

ESG is an integral part of our business processes. The respective ESG potentials are continuously analysed for each of the market areas. Find best practices for our sustainability-promoting lending here.

The former Postbahnhof has been transformed into a modern business location.

Investment loan 19,196 sqmThe automated processing of a large number of individual contracts for mobile leasing goods (bikes & e-bikes) is at the heart of this customer relationship.

Financing E-bikes EUR 60 millionBiodiversity forms the foundation for functional ecosystems worldwide, the stability of habitats, and enabling the renewal of natural resources. Intact nature therefore provides the conditions on which our society and its economic activities rely. Without stable ecosystems, supply chains, production, infrastructure, and longterm growth collapse.

For HCOB, this means that biodiversity is both an impact topic, because our financing activities affect nature, and a risk topic, as functioning ecosystems are essential for many economic sectors and therefore the profitability of HCOB’s clients. Biodiversity aspects are therefore firmly embedded in our credit process and form an integral part of the Sector Restrictions and the ESG scoring.